Introduction

Target Corporation, trading under the ticker symbol TGT on the New York Stock Exchange, has long been one of the most recognized and influential retailers in the United States. Known for its red bullseye logo and slogan “Expect More. Pay Less.,” Target has successfully carved out a niche between discount giants like Walmart and upscale department stores. Over the decades, Target has become not only a staple for millions of American households but also a significant player in the stock market, attracting both retail and institutional investors.

In recent years, the retail sector has undergone dramatic shifts fueled by e-commerce growth, supply chain disruptions, and evolving consumer preferences. Target has navigated these challenges with mixed results—sometimes demonstrating resilience, other times facing headwinds that impacted earnings and share price. For investors, the question remains: Is Target stock a buy, hold, or sell?

This article provides a comprehensive 4,000-word deep dive into Target stock, covering its history, financial performance, strategic initiatives, competitive landscape, and future outlook.

History of Target

Target’s origins trace back to 1902, when George Dayton founded the Dayton Dry Goods Company in Minneapolis, Minnesota. In 1962, the company opened the first Target store in Roseville, Minnesota, designed to combine the best of department store shopping with discount pricing. This concept quickly gained traction, and by the 1970s, Target had become a recognizable retail chain across the U.S.

In 2000, Dayton Hudson Corporation officially changed its name to Target Corporation, reflecting the dominance and brand power of the Target name. Unlike other retailers that struggled to find a unique identity, Target successfully positioned itself as a “cheap chic” retailer—offering stylish, quality products at affordable prices. This brand positioning distinguished Target from Walmart’s “everyday low prices” and Costco’s membership warehouse model.

Over time, Target expanded into groceries, home goods, apparel, and even exclusive designer collaborations, which have become a hallmark of the brand. The 2000s also saw Target experiment with international expansion, most notably in Canada, but that venture ultimately failed due to supply chain issues and was abandoned in 2015.

Despite setbacks, Target remained a household name in the U.S. retail landscape and continued to innovate in its approach to customer experience.

Target’s Business Model

Target operates as a general merchandise retailer, selling a wide range of products across categories such as:

- Apparel and accessories

- Home furnishings and décor

- Electronics and entertainment

- Groceries and household essentials

- Beauty and personal care

- Seasonal products

Unlike dollar stores or wholesale clubs, Target focuses on curating a shopping experience that blends affordability with aesthetics. This has been a major driver of its enduring popularity. Target often collaborates with designers and brands to create exclusive product lines that cannot be found elsewhere, increasing customer loyalty.

Another key pillar of Target’s model is its investment in omnichannel retailing. Recognizing the rise of e-commerce, Target has heavily invested in:

- Same-day delivery (via Shipt acquisition in 2017)

- Drive Up and Order Pickup services

- Target.com e-commerce expansion

- In-store digital integration

By blending physical retail with digital convenience, Target has attempted to stay competitive with Amazon and Walmart in the rapidly evolving retail landscape.

Target’s Financial Performance

Target’s stock performance has reflected both its successes and struggles. Let’s break down the financial aspects that investors care most about:

Revenue Trends

Target’s annual revenues have grown steadily over the decades, surpassing $100 billion in annual sales. The COVID-19 pandemic actually boosted Target’s revenues, as consumers relied on large retailers for groceries, home goods, and essentials. In 2020–2021, Target reported record-breaking sales growth.

However, in 2022–2023, Target faced challenges such as:

- Rising inflation impacting consumer spending habits

- Shifts away from discretionary purchases like electronics and home goods

- Increased theft and shrinkage impacting margins

- Supply chain costs squeezing profitability

Despite these headwinds, Target remains a top 10 U.S. retailer by revenue.

Earnings and Profitability

Target has maintained profitability for most of its history, though margins are relatively slim due to the nature of retail. Its operating margin typically ranges from 4–7%, compared to Costco’s razor-thin margins (around 3%) but lower than Amazon’s margin in its profitable AWS cloud segment.

Dividends and Shareholder Value

Target has a strong track record of dividend payments. It is a member of the S&P 500 Dividend Aristocrats, meaning it has increased its dividend for over 50 consecutive years. This makes it especially attractive to income-focused investors who prioritize steady, long-term returns.

In 2023, Target’s dividend yield hovered around 3–4%, making it one of the higher-yielding retailers compared to peers like Walmart. The consistency of dividend growth is a major selling point for TGT stock.

Balance Sheet and Debt

Target has managed its debt responsibly, though like most large retailers, it does carry significant liabilities. It continues to invest heavily in supply chain modernization, store remodels, and digital integration—all requiring capital expenditure. Still, its relatively strong free cash flow supports both dividends and stock buybacks.

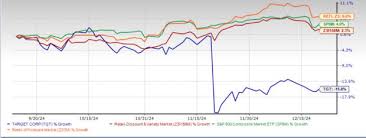

Target Stock Performance

Target stock has experienced both highs and lows.

- In the 2010s, Target stock steadily appreciated as the company expanded e-commerce, remodeled stores, and grew its dividend.

- During the COVID-19 pandemic (2020–2021), TGT surged to record highs, outperforming many retailers due to increased demand for essentials.

- By 2022–2023, TGT stock declined significantly as profits shrank amid inflation, inventory mismanagement, and broader retail sector challenges.

Despite volatility, Target stock has historically rewarded long-term holders. Investors who bought TGT a decade ago would still be sitting on substantial gains, plus dividends.

Competitors

Target operates in one of the most competitive industries: retail. Its biggest rivals include:

- Walmart (WMT): Walmart is Target’s largest competitor, dominating grocery and discount retail. Walmart’s scale and pricing power are unmatched, though Target has carved out a more “stylish” brand identity.

- Amazon (AMZN): Amazon poses the greatest threat in e-commerce. Target cannot match Amazon’s vast selection, but its omnichannel strategy provides an edge in same-day fulfillment.

- Costco (COST): Costco operates under a membership model and emphasizes bulk sales at low margins. Costco’s cult-like following is a challenge for Target, though the two serve slightly different markets.

- Dollar General / Dollar Tree: Discount retailers appeal to lower-income shoppers, especially in inflationary environments, eating into Target’s sales.

Target competes by focusing on brand loyalty, in-store experience, and design-oriented products that differentiate it from pure price competitors.

Strategic Initiatives

Target’s future depends on how effectively it executes its strategies:

- Omnichannel Integration: Target’s investments in Drive Up, Order Pickup, and Shipt are critical for competing with Amazon and Walmart. Convenience will remain a major driver of customer loyalty.

- Store Remodels: Target has been remodeling stores to improve aesthetics, layout, and digital integration, turning its physical locations into fulfillment hubs.

- Private Label Brands: Target has had great success with in-house brands like Good & Gather, Cat & Jack, and Threshold, which drive higher margins compared to third-party brands.

- Sustainability: Target has announced sustainability initiatives, including commitments to reduce carbon emissions and promote eco-friendly products. These efforts resonate with environmentally conscious consumers.

- Partnerships: Collaborations with designers, exclusive product launches, and partnerships (like with Ulta Beauty) help Target stand out in a crowded market.

Risks Facing Target Stock

Investors must weigh the risks before investing in TGT:

- Retail Sector Cyclicality: Consumer spending is highly sensitive to economic downturns. Recessions or inflationary environments hit retailers hard.

- Competition: Amazon, Walmart, and Costco pose constant threats. Failure to differentiate could erode Target’s market share.

- Shrinkage and Theft: Target has reported billions in losses due to theft and organized retail crime, which directly impacts profits.

- Supply Chain Costs: Global supply chain volatility increases costs and impacts inventory management.

- Political and Social Backlash: In recent years, Target has faced political controversies tied to product offerings, which can alienate certain customer bases.

- International Growth Limitations: Unlike Walmart or Amazon, Target has struggled to expand internationally, limiting its growth potential.

Future Outlook for Target Stock

Looking ahead, Target’s future will depend on balancing growth and resilience. Key themes include:

- Digital Growth: E-commerce penetration is expected to keep rising. Target’s digital channels must continue to scale profitably.

- Economic Conditions: If inflation moderates and consumer confidence improves, Target could see stronger discretionary spending.

- Dividend Reliability: Target’s dividend aristocrat status makes it appealing for long-term investors even in challenging times.

- AI and Technology: Incorporating AI in logistics, personalization, and supply chain management could improve efficiency and competitiveness.

- Store-as-Hub Model: Turning stores into fulfillment centers for same-day delivery could provide a durable edge over Amazon.

Long-term, Target is unlikely to dominate the retail world like Walmart or Amazon, but it can remain a steady, dividend-paying blue-chip stock with potential for modest growth.

Conclusion

Target stock (TGT) represents a fascinating case study in U.S. retail. With a rich history, strong brand, consistent dividends, and adaptability, Target has maintained relevance in one of the toughest industries. However, investors must consider the challenges: fierce competition, economic uncertainty, and shifting consumer behaviors.

For dividend investors, TGT remains a compelling choice due to its status as a Dividend Aristocrat. For growth investors, the upside may be more limited compared to tech-driven giants like Amazon. Ultimately, Target stock is best viewed as a long-term, stable investment that can provide steady returns and income while weathering the ups and downs of the retail sector.

At its core, Target’s strength lies in its ability to balance value, design, and convenience—a formula that has served it well for decades and will likely continue to shape its stock performance in the years ahead.